Caverton Offshore Support Group has returned to positive cash generation, signalling that its core operations are stabilising. However, the offshore logistics company remains trapped in losses as heavy finance costs continue to overwhelm improvements in operations.

The group’s audited financial statement for the period ended December 31, 2025, shows that while cash balances strengthened and liabilities declined, interest expenses of over N18 billion continued to erase operational gains, leaving shareholders with another year of losses.

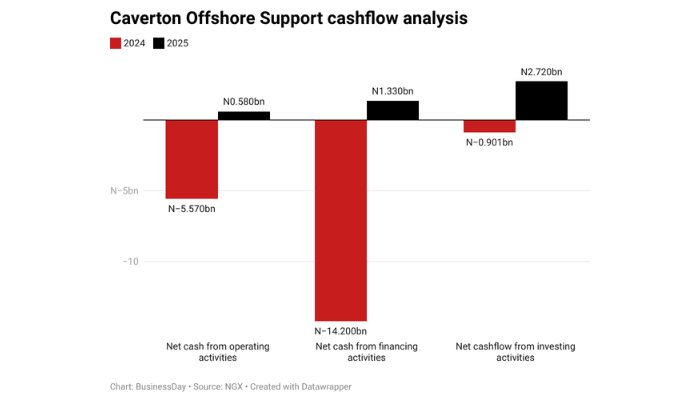

Perhaps the biggest positive surprise in the results is Caverton’s return to positive operating cash flow. Net cash generated from operating activities stood at N580.1 million in 2025, compared to a negative net operating cash of N5.58 billion in 2024.

During the period, working capital moved favourably, with trade and other receivables falling by N14.44 billion as collections improved, even as trade and other payables declined by N15.05 billion.

Investing activities generated N2.72 billion, against N900.7 million used in 2024. This came from N6.03 billion in proceeds from the disposal of assets previously held for sale and N12.21 billion in liquidated short-term investments, against N12.92 billion reinvested in new short-term securities and N2.36 billion in capital expenditure, mostly work-in-progress additions.

Financing activities added N1.36 billion, reversing N14.22 billion used in the prior year, as N35.64 billion in fresh borrowings drawn down outweighed N28.11 billion in principal repayments, N3.2 billion in interest paid, and N2.97 billion in lease payments.

Altogether, cash and cash equivalents rose by N4.66 billion during the year, against a N20.7 billion decline in 2024, taking the group from a net overdraft position of N1.39 billion at the start of the year to net cash of N3.26 billion at year’s end.

Revenue fell by 40%, but margins improved

Group revenue dropped to N24.1 billion in 2025 from N40.18 billion in 2024, a 40 percent decline. The fall was driven almost entirely by the aviation segment, where revenue slid to N22.58 billion from N38.5 billion. Within that, flight contract income more than halved to N7.74 billion from N20.03 billion, training services fell to N4.52 billion from N6.95 billion, and helicopter maintenance income dropped to N2.73 billion from N3.37 billion. Helicopter charter income held up better, falling only 6.8 percent to N7.6 billion from N8.15 billion. Marine revenue was broadly flat at N1.52 billion against N1.68 billion.

Despite the revenue collapse, gross profit rose to N12.15 billion from N8.42 billion, a 44 percent improvement. The cost of sales declined faster than revenue, down 62 percent to N11.96 billion from N31.76 billion, as crew salaries decreased to N5.46 billion from N10.73 billion, and consumables (including spares, aviation fuel, and freight) fell to N1.48 billion from N11.03 billion, reflecting a leaner cost base following the group’s scaled-down flight operations.

A N17.4 billion write-off drove administrative expenses higher

Administrative expenses nearly tripled to N28.99 billion from N10.49 billion, wiping out the gross profit gain. The single largest driver was a N17.42 billion loss on security deposits written off, tied to deposits paid on leased aircraft that the group could not recover after terminating the underlying lease agreements. Bank charges also rose sharply to N2.82 billion from N707 million, and a N263.8 million bad debt was written off during the year. Employee benefit expense within admin costs fell to N1.71 billion from N2.86 billion, consistent with a reduction in average headcount to 149 employees from 189.

Other gains flipped the operating line into profit

Where 2024 was hit by a N27.44 billion net loss on “other gains,” 2025 posted a N13.0 billion net gain, and this is where much of the year’s swing comes from. The components: a foreign exchange gain of N7.68 billion on translation of dollar-denominated exposures; a N3.35 billion gain from lease terminations; a N3.28 billion gain on settlement of long-outstanding liabilities, recognised after the group negotiated write-downs with creditors; and a N1.29 billion exchange gain specifically on borrowings, following the conversion of USD-denominated debt into naira at favourable rates. These gains were partly offset by a N2.6 billion revaluation loss on Caverton Marine’s property, plant and equipment.

Other income added a further N6.33 billion, up from N1.54 billion, driven chiefly by a N5.44 billion profit on the disposal of an aircraft previously classified as held for sale, once a lien placed on it by Access Bank was lifted. Government grant income (the amortised benefit of a below-market Bank of Industry loan) contributed N391.6 million.

Combined, these items contributed to a group operating profit of N3.6 billion, reversing a N30.96 billion operating loss in 2024.

Finance costs came in at N18.64 billion, down from N22.93 billion, but still the largest single expense line in the accounts. Interest on debts and borrowings rose to N15.82 billion from N5.22 billion, reflecting both a higher borrowing base and the elevated rates the group is paying on naira facilities, several of which carry interest of between 33 percent and 34 percent per annum. Interest on lease liabilities fell to N2.8 billion from N5.52 billion as the lease book shrank following terminations. Finance income remained small, at N358.1 million against N54.5 million, mostly interest earned on short-term bond investments and commercial paper.

Caverton’s 49 percent-held associate, Caverton Aviation Cameroon, contributed N806.8 million in share of profit, up from N165.3 million, on the back of a stronger performance at the Cameroonian unit.

Read also: Caverton explains delay in filing FY’25 results before regulatory due date

Loss before tax narrowed 74%

Loss before taxation came in at N13.87 billion, down 74 percent from N53.67 billion in 2024. After a tax charge of N13.8 million, loss after tax stood at N13.89 billion, against N53.86 billion the prior year. Basic and diluted loss per share improved to N4.11 from N16.00.

The improvement is real, but it should not be read as a return to profitability at the operating level; the swing owes more to non-recurring gains (FX, disposals, debt settlements) than to a recovery in the core aviation and marine businesses, both of which still posted losses.

Borrowing profile shifts toward short-term debt

The balance sheet shows that Caverton is actively restructuring its debt. Non-current borrowings fell 33.8 percent to N17.90 billion from N27.03 billion.

However, current borrowings almost doubled to N53.45 billion from N27.64 billion. The shift suggests a larger proportion of debt now falls due within one year, increasing refinancing pressure despite overall improvements in liquidity

Despite the revaluation surplus, Caverton’s shareholders’ funds remain underwater. Total equity improved significantly to negative N8.76 billion, compared with negative N54.61 billion in 2024.

The company has gained over 2.78 percent year-to-date on its share price, and it’s currently trading at N5.55 as of July 10th, with a market capitalisation of N18.6 billion

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp