Fuel Subsidy Removal and Nigeria’s Continuous Borrowing.

When President Bola Tinubu declared that “fuel subsidy is gone” in May 2023, it marked one of the most consequential economic decisions in Nigeria’s recent history. The administration argued that ending the costly subsidy regime would free trillions of naira annually for investment in roads, schools, hospitals, power infrastructure, and other public services. For many Nigerians, the expectation was clear: the immediate hardship would eventually translate into visible national development. More than two years later, however, that expectation remains largely unmet in the eyes of many citizens. Petrol prices have climbed to between ₦800 and over ₦1,000 per litre. Food prices continue to strain household budgets. Inflation remains stubbornly high, while the federal government continues to post significant budget deficits and accumulate more debt. The question now being asked in homes, markets, buses, and boardrooms across the country is both simple and legitimate:

“If subsidy savings were meant to strengthen public finances, why is government borrowing still accelerating?”

A Deficit That Continues to Expand

Nigeria’s fiscal numbers tell a sobering story. Federal revenue reached an estimated ₦21.5 trillion in 2024, the highest ever recorded. Higher tax collections, customs revenues, improved oil receipts, and the elimination of fuel subsidy all contributed to this increase. Yet government expenditure rose even faster, reaching approximately ₦35.9 trillion, leaving a deficit of around ₦14.4 trillion.

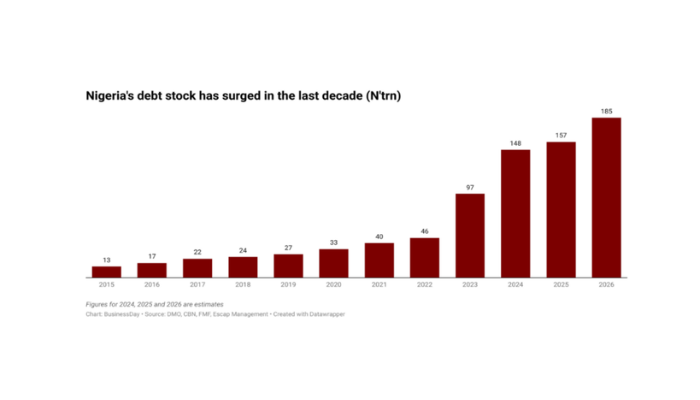

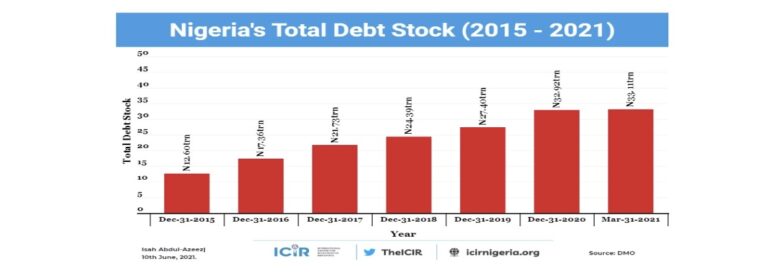

Simply put, for every ₦100 earned, government spent roughly ₦167. The difference was financed through borrowing. Nigeria’s public debt has consequently continued its rapid growth, from about ₦12 trillion in 2015 to approximately ₦97 trillion by 2023, before rising further to around ₦121 trillion by the end of 2025. Perhaps more concerning is the cost of servicing that debt.

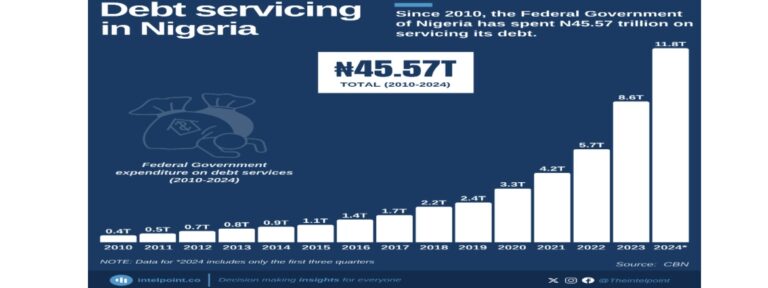

In 2024 alone, the federal government spent about ₦15.5 trillion servicing existing loans, an amount exceeding the combined allocations to education, healthcare, and public works.

That reality alone illustrates how debt is increasingly competing with development for scarce public resources.

The 2026 Appropriation Bill projects total expenditure of N68.32 trillion against revenues of N36.87 trillion, leaving a N31.45 trillion gap. This is 46.1% of the budget and well above the Fiscal Responsibility Act’s 3% GDP threshold. The government plans to finance N29.2 trillion through domestic borrowing, with the rest from projectlinked loans, asset sales, and aid.

Revenue Generation Lags behind Spending Growth.

Projected government revenue for 2026 is N36.87 trillion, expected from state-owned entities federation collections, independent revenues, and earnings from grants and special funds.

➢ N25.92 trillion from federation revenues

➢ N4.31 trillion from independent revenues

➢ N5.85 trillion from state-owned enterprises

➢ N1.37 trillion from grants and aid

➢ N300 billion from special funds

Despite improved revenue projections, windfall revenue due to increased crude price, expenditure growth has outpaced gains, contributing to the widening deficit and increased borrowing requirement. The gains from improved revenue generation is lost to growing debt servicing, as a result of continuous borrowing.

Why Subsidy Removal Did Not Deliver Immediate Fiscal Relief.

Many Nigerians assumed that removing subsidy would automatically reduce borrowing. The reality proved more complicated. While government revenue improved, the sharp depreciation of the naira significantly increased the cost of servicing foreign debt, importing goods, funding government operations, and executing infrastructure projects. A debt obligation that remained relatively unchanged in dollar terms became dramatically more expensive once converted into naira.

At the same time, government expenditure continued to rise. Implementation of the new national minimum wage, increased security spending, social intervention programs, and higher administrative costs absorbed much of the fiscal space created by subsidy removal. The anticipated savings did not disappear entirely—they were simply overtaken by rising expenditure elsewhere.

Following rising government borrowing, debt servicing remains one of the most significant pressure points in the 2026 budget framework. Debt service is projected at N15.81 trillion, making it one of the largest expenditure components.

▪ Domestic debt service: N10.16 trillion

▪ Foreign debt service: N5.36 trillion

Recurrent non-debt expenditure is estimated at N15.43 trillion, while capital expenditure stands at N32.29 trillion, reflecting a strong focus on infrastructure and development projects. Statutory transfers are projected at N4.80 trillion.

Too Much Spending, Too Few Visible Assets.

One of the greatest frustrations for many Nigerians is the limited visibility of what public borrowing has achieved. Although government expenditure approached ₦36 trillion in 2024, only about ₦7.9 trillion was allocated to capital projects. This means less than one-quarter of total spending went toward infrastructure and long-term investments, while the overwhelming majority funded salaries, pensions, overheads, debt servicing, and the day-to-day running of government. These are legitimate obligations, but they do not create the visible assets citizens expect to see. Compounding the challenge, many capital projects suffer delays arising from inflation, foreign exchange volatility, procurement bottlenecks, delayed releases of funds, and contractor financing constraints. Consequently, projects approved in the budget often remain incomplete long after their expected delivery dates.

Where the Borrowed Money Has Gone.

Contrary to the widespread perception that borrowed funds have simply disappeared, much of the debt has been used in identifiable ways. A significant share has financed annual budget deficits, covering recurrent expenditure such as salaries, pensions, and operational costs that government could not fully fund from revenue. Another portion has been used to refinance existing debt, replacing short-term, high-interest obligations with longer-term borrowing intended to reduce financing costs over time. Borrowed funds have also financed several major infrastructure projects, including railway expansion, highways, power projects, and social investment programs. Projects such as the Lagos–Ibadan Railway, Abuja–Kaduna Railway, the Siemens

Power Initiative, the Zungeru Hydroelectric Power Project, and the Lagos–Calabar Coastal Highway demonstrate that debt has contributed to development. However, Nigeria’s infrastructure deficit is estimated to run into tens of trillions of naira. Against such an enormous financing gap, even large-scale projects can appear insufficient relative to national needs.

Why Nigerians Struggle to See the Benefits.

The disconnect between government spending and public perception is driven by several factors. First, most public expenditure is directed toward recurrent obligations rather than long-term assets. Citizens cannot physically see debt servicing, pension payments, or administrative expenses. Second, inflation has significantly reduced the purchasing power of government spending.

Projects budgeted at one cost frequently require additional funding before completion because construction materials, diesel, imported equipment, and labour have become far more expensive. Third, project execution remains slow. Delays caused by inflation, funding constraints, procurement challenges, and foreign exchange shortages mean that many infrastructure projects take years before citizens experience their benefits. Finally, public communication remains weak. While government regularly announces allocations worth hundreds of billions of naira, citizens often lack access to clear information showing where projects are located, who is executing them, how much has been spent, and what progress has been achieved. In the absence of transparency, public trust inevitably suffers.

The Cost of Rising Debt.

Nigeria’s borrowing trajectory carries significant long-term implications. Debt servicing is consuming an increasing share of government revenue, leaving fewer resources available for healthcare, education, infrastructure, and other essential services. The need to generate additional revenue could also result in higher taxes over time as government seeks to strengthen its fiscal position. Heavy domestic borrowing has another consequence: it can crowd out private investment. Commercial banks often find government securities more attractive than lending to businesses, making credit more expensive and less accessible for entrepreneurs and manufacturers. At the same time, Nigeria remains exposed to external shocks. A significant decline in global oil prices or another sharp depreciation of the naira would further increase the cost of servicing foreign debt and place additional pressure on public finances. Although Nigeria is not currently facing a sovereign debt crisis, its debt-to-revenue ratio remains a source of concern for economists and investors alike.

Turning Borrowing Into Development.

Borrowing, in itself, is not a sign of economic failure. Virtually every developed economy has relied on debt at different stages of its growth. The critical issue is whether borrowed funds finance productive investments capable of generating future economic returns. Nigeria’s borrowing strategy should increasingly prioritise projects that expand economic productivity, power generation, transport infrastructure, ports, broadband connectivity, industrial parks, agriculture, and manufacturing. Government should also institutionalise greater transparency. Every project financed through borrowing should be publicly accessible through a digital portal showing its location, funding source, contractor, and project cost, implementation timeline, percentage completion, and periodic photographic updates. Such a system would strengthen accountability while restoring public confidence in public spending. Equally important is the need to reduce waste before increasing borrowing. Stronger procurement systems, implementation of audit recommendations, elimination of duplicated agencies, and more efficient public expenditure would reduce financing needs and improve fiscal sustainability.

The Bigger Picture.

The removal of fuel subsidy was a difficult but necessary policy decision. Few economists dispute that the previous subsidy regime imposed an unsustainable burden on public finances while encouraging inefficiency and market distortions. However, subsidy removal alone could never solve Nigeria’s fiscal challenges. Without broader reforms, including expenditure discipline, improved governance, faster project execution, stronger institutions, and greater transparency, the benefits of subsidy removal were always likely to remain limited. Nigeria is currently navigating a complex fiscal transition marked by legacy debt obligations, exchange-rate volatility, inflationary pressures, and rising recurrent expenditure. Until these structural challenges are addressed, borrowing will likely remain an important feature of fiscal policy.

Conclusion.

Nigeria’s public debt, now estimated at over ₦121 trillion, represents both an opportunity and a responsibility. If deployed efficiently, such borrowing can finance the infrastructure required to stimulate economic growth, improve productivity, create jobs, and enhance living standards. The challenge is not simply the size of the debt, but whether citizens can clearly identify the public assets and economic value created through it. Borrowing must translate into visible improvements, better roads, more reliable electricity, functional hospitals, quality schools, efficient transport systems, and stronger economic opportunities.

Ultimately, public confidence cannot rest solely on government assurances. It must be earned through transparency, measurable outcomes, prudent fiscal management, and a clear demonstration that every borrowed naira is delivering lasting value for Nigerians. Until that connection becomes evident, the question will continue to resonate across the country:

“Where is the money going?”

For more information, clarifications and support, Contact Prof. Prisca Ndu on +234 8033086190 or [email protected]

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp