For millions of Africans, the path to the internet did not run through a fibre cable or a laptop. It ran through an affordable Android handset priced somewhere between $80 and $150, bought at a roadside shop, activated on a local SIM, and used for everything from mobile payments to video calls. That price band quietly became one of the most consequential product categories on the continent. New data from global market intelligence firm Omdia now signals that this engine is losing power, and the timing could not be more consequential.

Omdia’s Q1 2026 African smartphone shipment report recorded total continental shipments of 19.9 million units, a 3% year-on-year increase compared to the same period in 2025. That headline figure suggests stability. The detail beneath it tells a more complicated story.

TechCartel, which has closely followed the trajectory of smartphone affordability across Nigeria and the broader continent, breaks down what the latest numbers reveal and what they mean for the millions of Africans whose first experience of the internet runs through a budget device.

The continental average is being held up by a small number of markets performing well, while several others are contracting sharply. South Africa recorded a 17% year-on-year increase, the best performance on the continent, driven by consumers upgrading to higher-specification devices and a significant distribution push by HONOR into the upper mid-range segment. The average selling price of a smartphone in South Africa climbed 4% to $369. Nigeria added 8% year-on-year, with growth concentrated in the $200 to $299 price tier. With persistent inflation and rising mobile data costs putting pressure on household budgets, Nigerian consumers showed a clear willingness to stretch spending in order to secure reliable 4G and 5G connectivity. Morocco recorded a 6% increase, helped by a government decision to cut import duties from 17.5% to 2.5%, a policy shift that improved device affordability at the retail level.

Other markets told a harder story. Algeria recorded the sharpest continental decline, down 28% year-on-year, hit by strict government import regulations, foreign exchange shortages, and stalled progress on localised manufacturing. Kenya fell 16%, with consumers choosing to extend the life of existing handsets instead of upgrading at prices that had moved beyond comfortable reach. Egypt dropped 10%, pressured by weakened domestic consumer sentiment and supply chain disruptions tied to geopolitical tensions across the broader Middle East.

The Squeeze on Africa’s Entry-Level Device Tier

The more significant story in Omdia’s data is not geographic. It is about what is happening to the price bands that African consumers have historically relied on most.

The sub-$200 segment accounted for 75% of total smartphone shipments in Q1 2026. Africa’s market has always been built on volume at the entry tier, and that has not changed. What has changed is the cost base underneath it. Rising prices for memory, NAND storage, and semiconductor components are pushing manufacturers to reprice their portfolios upward. The $300 to $499 mid-range segment expanded by 43% in Q1 2026, partly due to this repricing and partly driven by the growing availability of device financing programmes. For the vast majority of African consumers, however, a device in that price band remains out of reach.

Omdia projects a 28% contraction in the sub-$200 segment for the full year of 2026, with the $80 to $150 tier absorbing the heaviest pressure. As compressed vendor margins make it harder to produce affordable devices without passing costs on to consumers, the floor of the market is rising. The people closest to that floor are the first ones priced out.

The Q1 growth figure also deserves closer scrutiny. A portion of it was not driven by fresh consumer demand but by manufacturers front-loading inventory during the quarter, importing extra stock early to outrun rising component costs and currency instability. That early push flattered the Q1 numbers, and the quarters ahead are starting from a thinner base than the opening data implies.

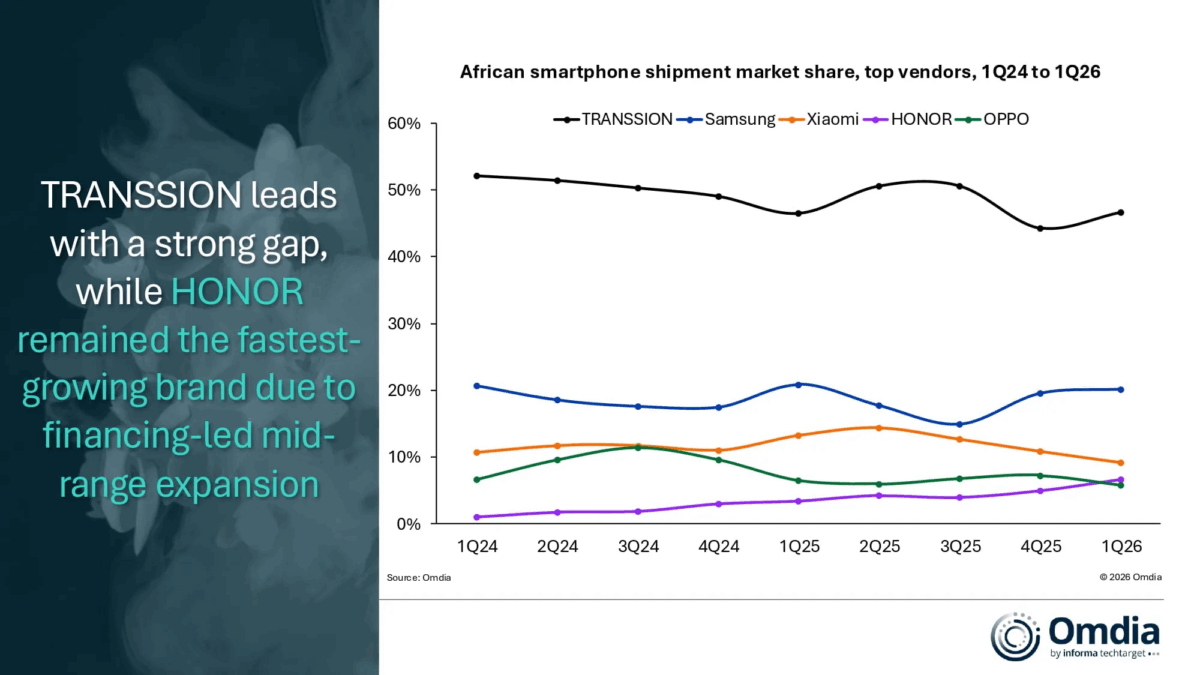

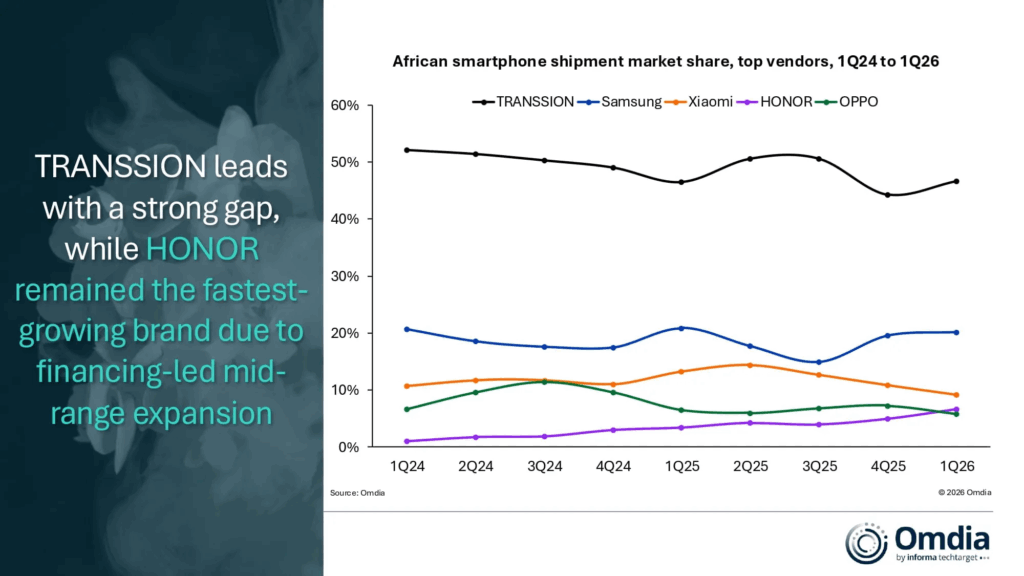

Across the vendor market, the same cost pressures are producing very different outcomes. TRANSSION retained continental market leadership with a 47% share and 4% year-on-year growth. Its three sub-brands, Tecno, Infinix, and itel, cover distinct price points within the entry tier, giving the group broad reach across the budget segment. Its last-mile distribution networks and localised manufacturing operations provide a buffer that brands dependent on imports do not have. HONOR posted the highest growth rate of any major vendor, up 101% year-on-year, driven by mobile operator partnerships in South Africa and device financing options that expanded access to higher-specification handsets. Samsung logged a marginal 1% decline but held its ground in the $150 to $299 segment through the Galaxy A series. Xiaomi, whose continental portfolio spans its main line and the POCO sub-brand, dropped 28% year-on-year as memory supply shortages hit its entry-tier offering hard. OPPO fell 7%, affected by operational restructuring and a difficult performance in Egypt.

Omdia is explicit about what will separate brands that manage the second half of 2026 from those that do not: established financing ecosystems, mobile operator partnerships, localised manufacturing capacity, and last-mile distribution depth. The brands that built those foundations before the squeeze arrived are in a far stronger position than those that did not.

The appetite for connectivity across Africa has not weakened. A continent with a young, growing population and an expanding digital economy continues to push more people toward mobile internet every year, and smartphones remain the primary vehicle for that access. What is changing is the accessibility of the devices that have historically served as the entry point to that access. If the $80 to $150 tier contracts as sharply as Omdia projects, the next wave of first-time smartphone users will wait considerably longer than the industry had anticipated.

Across the continent, mobile access sits at the foundation of how people bank, learn, trade, and communicate. A shrinking affordable device tier is not an abstract market correction. It is a direct setback for the millions of people whose participation in the digital economy depends on a phone they can actually afford to buy. The affordability conversation in African tech has been had many times before. The data now suggests it can no longer be deferred.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp