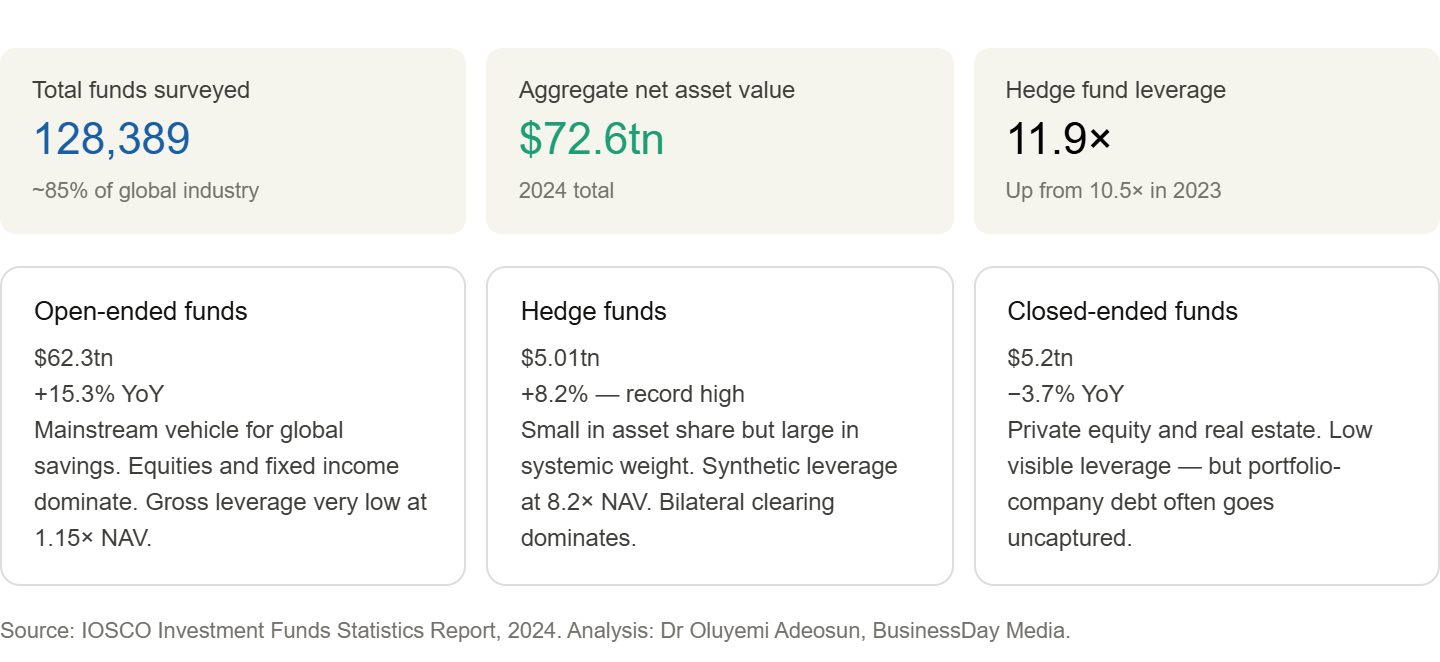

The latest IOSCO Investment Funds Statistics Report offers a useful reminder that size and stability are not the same thing. The global investment fund industry covered in the survey reached 128,389 funds with aggregate net asset value of $72.6 trillion in 2024, representing roughly 85 percent of the global funds industry.

That is a striking number in itself, but the more important point is what sits beneath it: a world in which assets continue to gather at scale, risk remains unevenly distributed, and the plumbing of modern finance still leans heavily on a relatively small corner of the market. What the report shows is not a system in obvious distress. On the contrary, the broad picture is one of expansion with relatively steady aggregate risk. Open-ended funds and closed-ended funds, which together account for the overwhelming majority of assets, continued to grow in number, while open-ended funds posted a strong rise in net asset value. Hedge funds, though much smaller in asset share, remain disproportionately important because they carry far more derivatives activity and materially higher leverage than the rest of the fund universe. That asymmetry matters. It means the most systemically relevant pressure points may not be where the bulk of the money sits, but where leverage, synthetic exposures and market interconnectedness are most intense.

The industry is expanding, but not evenly

The headline growth numbers are impressive. Open-ended fund assets rose by 15.3 percent to $62.3 trillion in 2024, while qualifying hedge fund assets climbed 8.2 percent to a record $5.01 trillion. Closed-ended fund assets, by contrast, slipped 3.7 percent to $5.2 trillion, though they remain far above earlier-decade levels. In other words, the industry is still moving forward, but the drivers are different across segments. Open-ended funds are benefiting from growth in mainstream markets and investor participation, while closed-ended funds are navigating valuation adjustments, reclassifications and the slower-moving logic of private assets.

That divergence tells policymakers and investors something important. Public-market vehicles remain the centre of gravity for global savings mobilisation, especially through equity and fixed-income funds. But private-market structures are becoming more structurally embedded, particularly in real estate and private equity. The consequence is that regulators can no longer view the fund industry through a single lens. Liquidity, valuation, transparency and leverage risks behave very differently in a daily-dealing bond fund than in a private equity vehicle with long lockups and opaque underlying leverage. The report wisely avoids flattening those distinctions, and that is one of its biggest strengths.

Hedge funds are still the sharp edge of the system

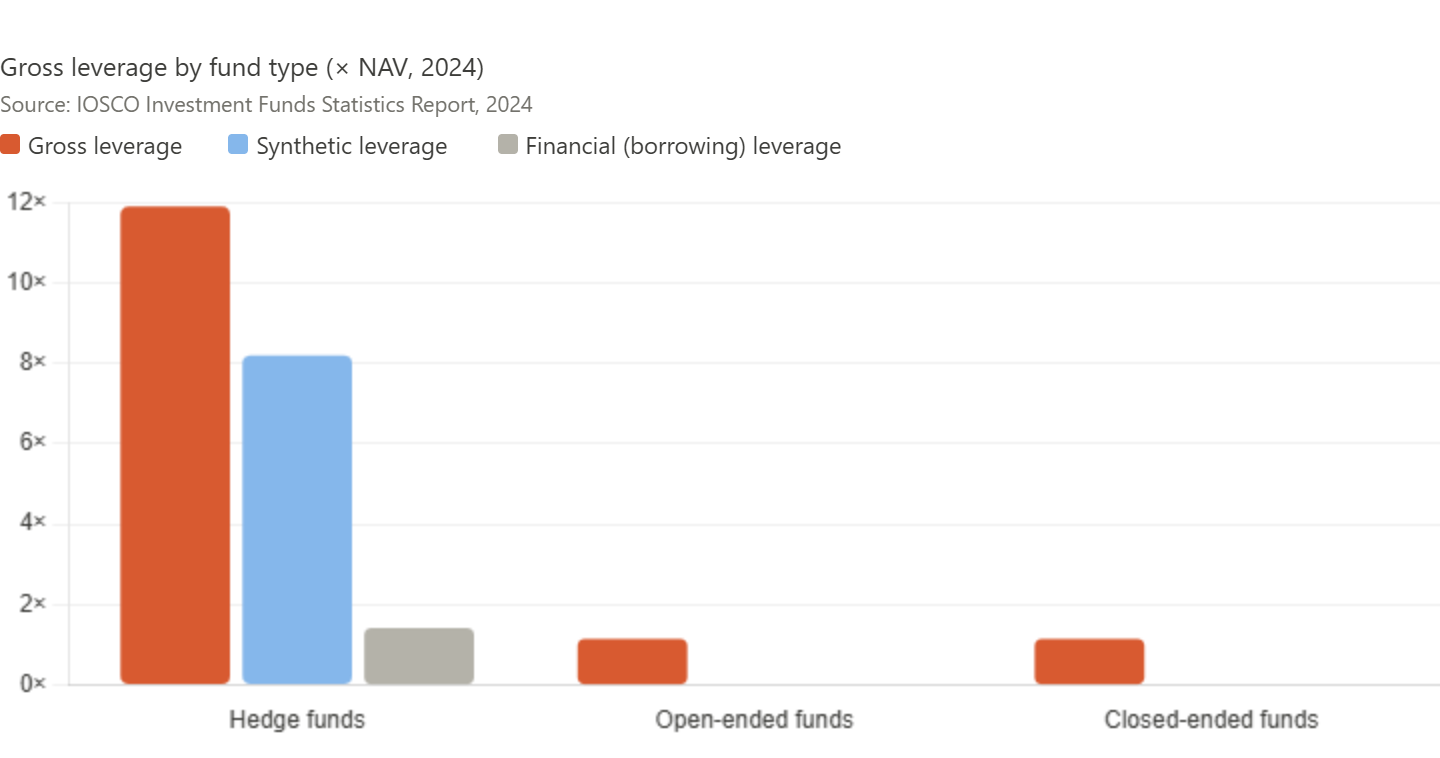

If there is one part of the report that deserves especially close reading, it is the hedge fund section. Hedge funds remain small relative to the full industry, but they are where leverage and derivatives usage are concentrated. IOSCO shows gross hedge fund leverage at 11.9 times NAV in 2024, up from 10.5 times in 2023, while synthetic leverage rose to 8.2 times NAV. Borrowing also increased, with total financial leverage reaching 1.42 times NAV. These are not crisis numbers in themselves, and they remain below earlier peaks, but they point to a sector that is once again leaning more heavily on borrowed balance sheets and derivative structures.

The composition of exposures also matters. Hedge fund activity remains heavily concentrated in sovereign bonds, listed equities, reverse repos and cash, while derivatives exposures are dominated by interest-rate contracts, followed by foreign exchange and equity derivatives. That combination says a great deal about how modern macro and relative-value strategies are being expressed. It also means that stress in sovereign bond markets, funding markets or rate volatility can be transmitted quickly through highly active, highly leveraged portfolios. For governments and regulators, that is the policy takeaway: the question is not simply whether hedge funds are growing, but whether their growing exposures are becoming more entwined with core market functioning.

The calmer majority should not breed complacency

By comparison, open-ended and closed-ended funds look far more restrained. Open-ended funds posted gross leverage of 1.15 times NAV, with borrowing and financial leverage described as very low in aggregate. Their portfolios remain dominated by equities and fixed income, while derivatives usage is mainly linked to interest-rate and foreign-exchange risk management rather than aggressive balance-sheet expansion. Closed-ended funds also appear conservative at fund level, with gross leverage of 1.15 times NAV and derivatives usage still modest. Their portfolios are concentrated in private equity, real estate and other alternative assets, which naturally reflect a longer holding horizon.

Still, low visible leverage should not be mistaken for low underlying vulnerability. IOSCO is careful to note that some closed-ended fund data may understate true leverage because private equity structures do not always capture leverage borne at the portfolio-company level. That caveat matters enormously. In today’s markets, leverage is often migrating away from the fund shell and into the underlying asset or financing structure. Investors who rely only on top-line fund leverage may therefore miss where real fragility sits. That is a warning both for supervisors and for institutional allocators who increasingly rely on private markets for yield, diversification and long-term return enhancement.

Geography reveals where capital still prefers to live

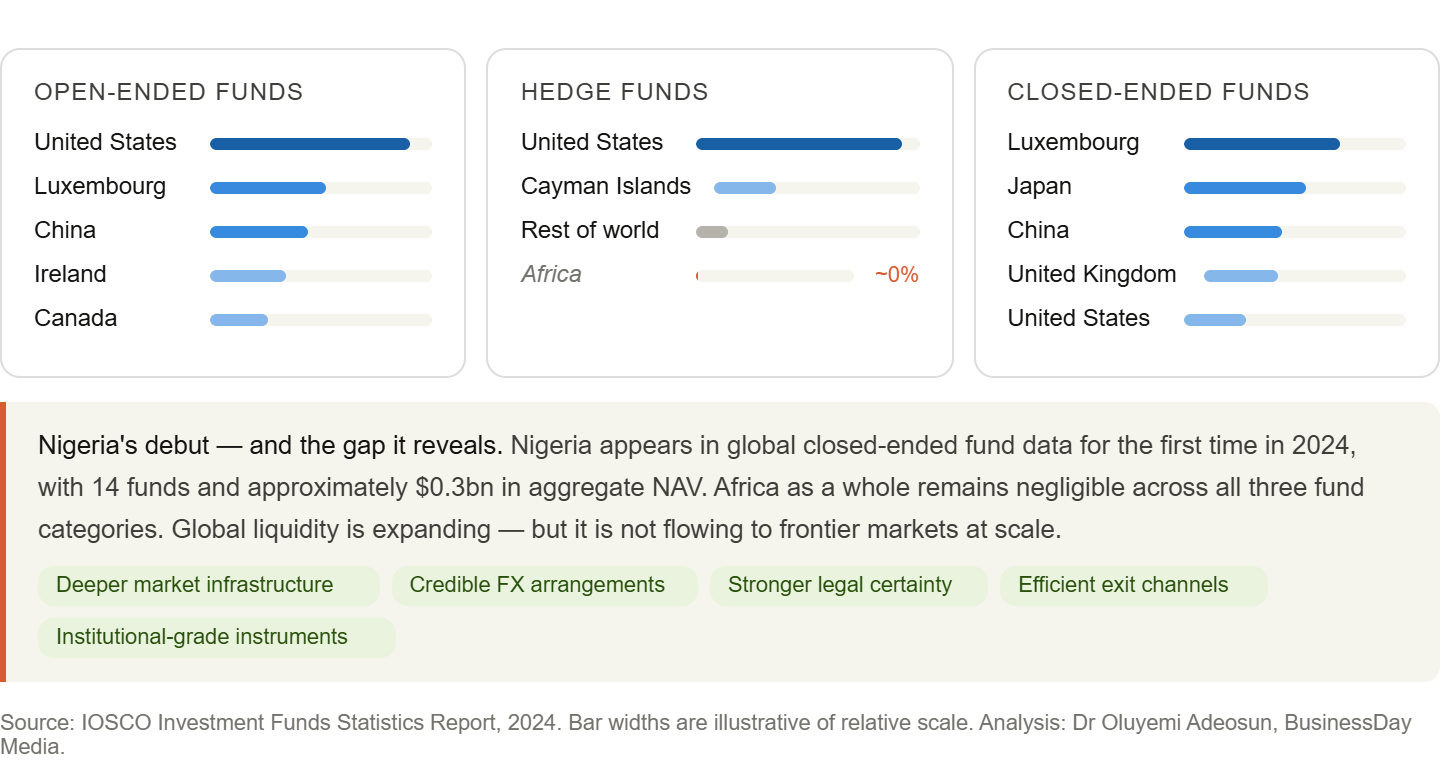

The report also confirms how concentrated global fund activity remains. Open-ended fund assets are led overwhelmingly by the United States, with sizeable roles for Luxembourg, China, Ireland and Canada. Hedge fund assets remain heavily dominated by the US as well, while closed-ended fund activity is anchored by Luxembourg, Japan, China, the UK and the US. Geographically, allocations continue to favour North America and Europe, with Asia-Pacific gaining ground, but Africa remains marginal across most categories. For instance, hedge fund geographical allocation to Africa is negligible, while open-ended and closed-ended funds also devote only a tiny share to the continent. Nigeria appears in the report for the first time in closed-ended funds, but with only 14 funds and about $0.3 billion in aggregate NAV.

This is where the report becomes especially relevant for emerging markets. Global liquidity is expanding, but it is not naturally flowing toward frontier or underserved regions at scale. That has implications for African governments, capital-market operators and organised private sector groups. If domestic markets want a larger share of global portfolio and private capital, they must do more than court investors rhetorically. They need deeper market infrastructure, better fund reporting, stronger legal certainty, credible FX arrangements, efficient exit channels and investable instruments that meet institutional standards. Capital goes where transparency, liquidity and enforcement are strongest. Sentiment matters, but market architecture matters more.

What governments, investors and the private sector should do now

For governments, the first imperative is not to smother capital formation with blunt rules, but to strengthen surveillance where leverage, derivatives concentration and bilateral counterparty exposures are highest. IOSCO’s findings show that bilateral clearing still dominates derivatives activity across hedge funds, open-ended funds and closed-ended funds. That means policymakers should keep improving data quality, collateral transparency and stress-testing capacity around non-bank finance, especially in rate, FX and repo-linked markets. A second priority is to accelerate reforms that make domestic capital markets investable at scale, particularly in emerging economies that remain under-allocated in global portfolios.

For investors, the message is to separate headline growth from underlying structure. Bigger funds are not necessarily safer funds, and low disclosed leverage does not always mean low embedded risk. Allocators should pay closer attention to liquidity terms, derivative concentrations, redemption structures and exposure to markets where volatility can reprice leverage suddenly. For organised private sector players, especially pension funds, insurers, corporates and market intermediaries, the opportunity is to help build deeper local ecosystems: better issuance pipelines, improved governance standards, co-investment platforms and more credible vehicles for long-term domestic savings. The future of fund growth will not depend only on how much money the world has. It will depend on whether institutions can direct that money into markets that are not only large, but genuinely resilient.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp