Nigeria’s external reserves owe much of its growth to the development at the international crude oil market. Other sources of impact in external reserves include foreign remittances and loans. In other words, a positive development at the international crude oil market, all other things being equal, will signal a similar development in the nation’s foreign exchange reserves. That is, a surge in crude oil prices will bring about a noticeable increase in Nigeria’s external reserves.

Crude oil prices have trended upwards since the beginning of the year. From $50.24 a barrel on December 31, 2020, the price of OPEC basket on October 15, 2021 hit $83.54 a barrel, an increase of 66 percent when compared with its price last December.

Many factors could be attributed to the positive sentiment in the global energy market, and one of these factors being economic recovery countries are experiencing now because of the concerted efforts on vaccination. This has raised people’s hope that the world will overcome COVID 19 pandemic sooner than later.

Nigeria is, directly and indirectly, benefiting from the rising crude oil prices, although the opportunity cost is also high in the sense that the high subsidy regime has prevented Nigeria from having enough resources to execute some crucial projects and consequently, more foreign loans have to be sought.

In July 2021, the Minister of Finance, Budget and National Planning, Zainab Ahmed said Nigeria incured on average N150 billion in subsidy payment on monthly basis. In 2019, the federal government set aside N305 billion for subsidy payments.

At the current crude oil prices, the landing price of PMS is put at about N290 per litre, and with average monthly PMS consumption of 45 million litres, a whopping N7 billion leaves Nigerian covers in the name of subsidy payment on a monthly basis.

In 2020, when crude oil prices were not as high as in the current regime, Nigeria spent N2.34 trillion on debt servicing out of N3.25 trillion revenue generated in the country. In 2019, debt servicing gulped N2.11 trillion out of N3.86 trillion revenues generated in the federation, implying that debt servicing gulped 72 percent of the revenue in 2020, and 54.7 percent in 2019. Removal of subsidy could have reduced the need for huge external loans and thus saves the country more resources to develop critical infrastructures.

Read also: Excess crude account slumps to lowest despite oil rally

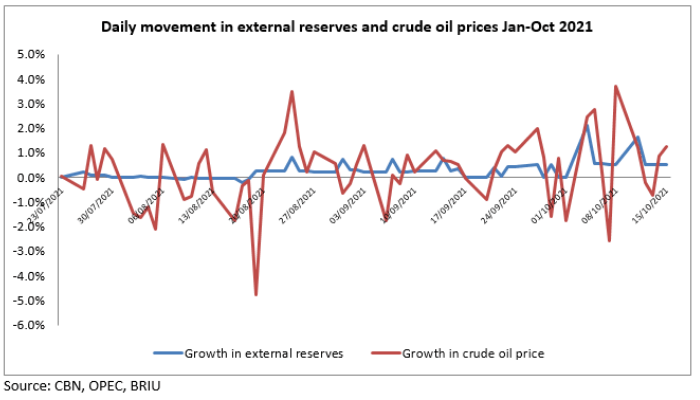

Nigeria’s external reserves, the liquidity segment, added $4.54 billion between December 2020 and October 15, 2021, indicating a growth of 13 percent during the period. In other words, the external reserves rose from $35.04 billion to $39.6 billion.

Growth in external reserves was significant on two days in the month of October. On October 4, 2021, external reserves rose by 2.1 percent to $37.3 billion, up from $36.5 billion on September 30, 2021. With an additional $787.6 million added on that day alone, this remains the highest accretion to external reserves since December 2020. Similarly, crude oil prices rose by 2.5 percent on the same day to close at $78.26 a barrel.

Another day of significant accretion was October 11, 2021 when $621.8 million was added to external reserves and that raised the liquid portion of external reserves to $38.8 billion on that day. Trend in crude oil prices showed there was a build up to the huge accretion to external reserves on October 11. On October 8, crude oil prices recorded a daily upswing of 3.7 percent to $81.54 per barrel. It further rose by 1.2 percent on October 11 to $82.53 a barrel.

Monthly accretion to external reserves indicated there was a boost to the confidence of the Central Bank of Nigeria (CBN) as oil prices rose. In October 2021, the average daily accretion to external reserves was $304.35 million. It was $103.13 million in September 2021; $27.15 million in August 2021, $1 million in July, $4 million in April, and $45 million in January 2021.

Conversely, there was depletion in external reserves in other months, and most probably to meet the exigencies of the day. In February, the average depletion in external reserves amounted to $55.8 million, $10 million in March, $34.9 million in May and $21 million in June.

Different reasons were adduced to the decline in external reserves in the aforementioned months, which ranged from a decrease in foreign exchange from other sources such as non-oil revenues and the repayment of $500 million Eurobond that reached maturity early in the year.

Options available to CBN

- US Lawmakers write Justice Department to re- investigate Nigeria’s $1.3 billion oil-field scandal

- Nigeria plans crude oil trading on Lagos exchange for first time to open access to funding for industry

- Aelex Notes: “Critical considerations for the implementation of domestic crude supply obligations under the PIA”

Reduce trade deficit

One of the options is to reduce the country’s trade deficit since inflows through higher exports have the potential to bolster the country’s external reserves. In 2018, Nigeria’s trade balance was N5.4 trillion but that slowed to N2.2 trillion in 2019. Due to obvious reasons such as the pandemic and associated shutdowns of the global economy, Nigerian trade deficit surged to N7.4 trillion in 2020. At the end of the second quarter ended June 2021, Nigeria’s trade deficit was N5.8 trillion.

While the argument of the pandemic is still tenable, it should be noted that some countries recorded trade surpluses in 2020. According to the Economic Times of India, a number of countries within the Indo-Pacific trading bloc recorded trade surpluses last year. The member countries are Australia, Bangladesh, Chile, Colombia, France, Fiji, India, Indonesia, Japan, Kenya, South Korea, Maldives and Mauritius

Others are Malaysia, Mexico, Singapore, Sri Lanka, Thailand, Vietnam, the United Arab Emirates (UAE) and the United States of America (USA). Collectively, they controlled 62 percent of the global GDP and 50 percent of the World’s trade.

Meanwhile, in 2020 Bangladesh’s trade surplus was $6.88 billion; $2.53 billion for Sri Lanka, $1.89 billion for Kenya, and $1.36 billion for France. Interestingly, 2020 was a unique year for China as it recorded $535 billion in trade surplus.

Nigeria needs to curate sector-specific export incentives to raise the level of the country’s non-oil exports. Still dominated by primary produce, even at that, the problem of rejection of primary produce in the European market speaks volumes, and urgently requires stakeholders in the sector to think out of the box.

Attract foreign investments

Investors are looking for countries that offer them better returns on investments in emerging economies and Nigeria stands to benefit from the rising investors’ appetite. Natural endowments, the big market and the low cost of labour are Nigeria’s attractive features. We must maximise these optimally.

This is as two investment-focused reports, recently released on the attractiveness of African economies, gave Nigeria different ratings. The lack of consistency in the two reports could make investors get cold feet towards Nigeria.

The first report in 2021 by the Rand Merchant Bank (RMB), tagged “Where to Invest” placed Nigeria outside of the ten most attractive countries in Africa for investment. Instead, the RMB report listed Egypt, Morocco, South Africa, Rwanda, Botswana, Ghana, Mauritius, Cote d’Ivoire, Kenya and Tanzania in that order as the most attractive countries to invest.

A key indicator, according to RMB, was fiscal score measuring the size, nature and efficiency of government fiscal measures to strengthen resilience in the midst of the COVID-19 lockdown in major markets across Africa. In 2020, Nigeria was ranked seventh on the RMB’s “Where to Invest” report.

The latest report portrays Nigeria in good light, and that is the Absa Africa Financial Markets Index 2021 report. Nigeria was ranked third after South Africa and Mauritius as the most attractive countries to foreign investment, for performing well in the attractive regulatory and market environments.

Notwithstanding, the report sounded a note of warning to Nigeria because while it scored 65 points in 2020, its score fell to 63 points in 2021 slightly above Ghana’s which scored 62 points. This signals that if nothing meaningful is done to improve on that two parameters-regulatory environments, and the market environment, Nigeria may be dethroned next year by either Ghana or Uganda.

In addition, other parameters where Nigeria performed poorly must be improved upon. On access to foreign exchange, Nigeria scored 20 points, just as it also scored 44 points on the capacity of local investors.

“Nigeria continues to perform poorly in this pillar. It imposed administrative controls by expanding the number of goods subject to import restrictions, enforcing existing export repatriation rules and restricting FX supply to certain windows.

“While these measures restricted capital outflows and helped keep reserves stable, market liquidity remained below pre-pandemic levels. Due to the control measures and global macroeconomic imbalances, foreign portfolio investors’ appetite remained subdued. The volatile FX market and the delays in the repatriation of foreign currency out of Nigeria caused further problems”, the Absa report stated.