In early 2018, Chinua Azubike, CEO of Infrastructure Credit Guarantee Company, Ltd (Infracredit) sat immersed in thought in his office on Victoria Island in Lagos, Nigeria. Infracredit, a fledgling company established and sponsored by the Nigeria Sovereign Investment Authority (NSIA)A, in collaboration with Guarantco,b was attracting plenty of interest for its innovative and potentially transformative credit enhancement product. But to grow as quickly as planned and have the impact the company’s board members and shareholders expected, Azubike would have to rapidly increase the size of Infracredit’s balance sheet. Capital could come from new equity, additional debt, or increased credit guarantee commitments from third parties. All three choices were difficult routes and all three paths involved control and dilutive aspects. If Azubike selected well, Infracredit could transform the face of power, roads, ports, water and more across Nigeria and sub-saharan Africa. If he chose poorly, an elegant idea (and a lot of work and reputations) would come crashing down.

Infracredit was a quasi-private credit enhancement entity formed to address infrastructure finance deficits in Nigeria. The so-called “infrastructure finance gap” was a problem for government and society in Nigeria as in many parts of the world. Infrastructure projects like power plants and dams were very large capital investments that could generate long-term consistent cash flows, but their financing and delivery involved multiple risks and uncertainties. If funds came from traditional international sources like the World Bank or African Development Bank, those lenders would worry about foreign exchange, interest rates, and political risk and would almost always seek sovereign guarantees (payment guarantees from the federal government). Such assurances and guarantees were hard to come by, difficult to negotiate, and project inception could take decades. Nigeria needed power, water, roads, and ports faster than that.

Nigeria had recently reformed its pension administration system so that entities like ARM Pensions (ARM), Stanbic IBTC Pension Managers (Stanbic), and the Nigeria Police Force Pensions Limited (NPFP) could both accept significant amounts of retirement funds from workers and also, more importantly, manage and invest those funds in a transparent and safe structure. Fund managers acted as professional fiduciaries for the benefit of the retirees. One of the asset classes in addition to government bonds, equities, and corporate bonds that was authorized for investment by pension funds was infrastructure debt securities.

Other entities took different approaches to raise capital for infrastructure in this market. Africa Plus Partners (Africa Plus), for example, proposed a fund structure with features of American private equity. In January 2018 Africa Plus completed its first fund close, raising 12 billion Naira (approximately US$ 33 million). It was not yet clear if this type of fund arrangement would be as attractive as debt for pension fund investors.

Until recently, few Nigerian infrastructure securities had strong enough credit ratings to be investable by cautious pension funds. Infracredit hoped to break that logjam by supporting infrastructure issues denominated in local currency with credit assurances taking the place of sovereign guarantees. Clearly this concept had the potential to change the nation in a positive way. Could Infracredit become a very large player? If the model was proven, could it be replicated in other nations? What would be the conditions precedent to make other nations attractive for an Infracredit model? Azubike thought about these options and how to get from here to there.

Nigeria at a Glance

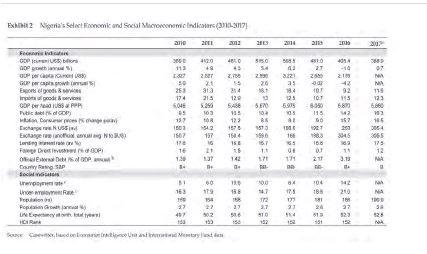

Nigeria was located on the west coast of Africa along the Gulf of Guinea bordered by Benin, Chad, Niger and Cameroon (see Exhibit 1). With its multi-ethnic and multilingual population of approximately 191 million, the country had the largest and most diverse population in Africa.1 This size, together with its gross domestic product (GDP) of US$389 billion, abundant oil reserves and strategic international linkages, made Nigeria one of the most important nations on the African continent (see Exhibit 2).

For almost forty years after independence from Britain in 1960, Nigeria experienced a turbulent period characterized by successive military coups, ethnic conflict, civil unrest and instability. The adoption of a new constitution in 1999 marked the beginning of a sustained period of democratic governance and significant economic progress for the country. Beginning in 2000, Nigeria enjoyed fifteen years of sustained economic growth. In March 2015 through a largely fair and peaceful democratic process, Nigeria elected a member of the opposition All Progressives Congress party, Muhammadu Buhari, as president. This marked the first time in the nation’s history that power was peacefully transferred from the long-standing party in power to the opposition.

In 2016 Nigeria fell into recession largely due to a major worldwide slump in prices for oil, which had been the nation’s largest source of government revenue and its greatest focus of foreign direct investment (FDI).3 In addition, other sectors including services, agriculture and industry that had become the main engines of the country’s non-oil economic expansion contracted significantly due to a weakening global economy.4 The subsequent reduction of government receipts, combined with currency fluctuations, all wreaked havoc on the country’s economy.5 By the end of 2017, GDP had declined from US$ 405 billion in 2016 to US$ 389 billion and the Nigerian Naira remained at historic lows against the US dollar6 (see Exhibit 2).

READ ALSO:Housing Estates in Lagos reel from lack of infrastructure

The deteriorating economic situation placed severe strains on public finances, limiting the government’s ability to invest in much-needed infrastructure, address widespread corruption, deal with security, and institute important policy reform.7 Access to finance became more difficult as banks suffered capital restrictions.

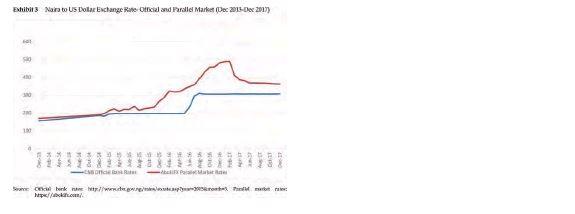

8 The subsequent reduction of government revenue resulted in the percentage of unemployed and underemployed together reaching 35.2% in 2016 and inflation rising to 16.5% in 2017 (see Exhibit 2). While the Naira was officially pegged to the US dollar, during the recession the government often restricted access to foreign exchange to prevent currency devaluation. Due to the scarcity of dollars in the official market, businesses resorted to buying the US currency on the parallel market, resulting in a spread of as much as 60% in February 2017 between the official and unofficial rates (see Exhibit 3).

Nigeria came out of recession in 2017. However, the government continued to struggle to stabilize the economy and find a more robust path to economic growth. The country faced additional uncertainty due to factors including President Buhari’s ill-health and related long absences from the country, public security issues (in particular, Boko Haram violence and lawlessness in the north), ethno-nationalism in oil producing regions, and renewed secessionist tensions in Biafra.9 Although observers viewed the country’s democracy as sufficiently robust to survive this potential instability, elections planned for 2019 remained a source of uncertainty.10

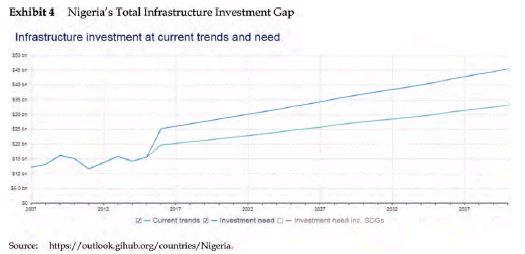

Infrastructure Finance in Africa Across Africa, a large and growing differential existed between actual infrastructure investment and the amount needed to adequately support the continent’s increasing population, rapid urbanization and expanding economic growth. In a joint report issued in May 2017, the Boston Consulting Group and the Africa Finance Corporation (AFC) estimated Africa’s annual infrastructure finance gap to be approximately US$100 billion. Nigeria, the nation with the largest population on the continent, accounted for a sizable portion of this shortfall.11 According to the country’s own National Integrated Infrastructure Master Plan (NIIMP), the amount required to meet Nigeria’s infrastructure related investment needs was US $3 trillion over a thirty-year period12 – or $100 billion per year for Nigeria alone. Estimated infrastructure spending required to meet the country’s preferred growth plan (the ‘accelerated path’) would need to increase several fold from US$5-$25 billion per year in 2014-2018 to many times that amount – and even more going forward.13 See Exhibit 4 for an illustration of Nigeria’s total infrastructure investment gap projected to 2037.

The power sector in Nigeria (as in much of Africa) faced a particularly large mismatch between required generation and existing supply. According to Azubike quoted in The Sun newspaper,

Nigeria’s aggregate electricity need has been estimated at about 160,000 MW to satisfy the local electricity demand. With an installed capacity of 12,132 MW, only an estimated 7,000 MW of installed capacity is operational. Of this, only between 3,000 MW and 5,000 MW are actually being generated due to unavailability of gas, breakdowns, water shortage and grid constraints, which have led to acute shortage of power across the country. Nigeria’s transmission grid is estimated to cover a maximum 40 per cent of the country, with annual self-generating capacity outside the national grid put at over 15,000 MW.14

This implied that more electricity was self-generated by households, businesses, and institutions on their own than was supplied by the utility company – a quite inefficient and unusual situation in the minds of many observers.

Global electricity generating capacity, and usage, varied substantially. With a population of about 325 million, the United States used about 12,000 kwh per person per year. Nigeria’s population of about 191 million used about 129 kwh per person of electricity per year. In Africa, Egypt’s 97 million people sources of private funding (notably banks) were increasingly constrained by the global financial crisis and new more stringent capital requirements imposed by banking regulations, including Basel III capital adequacy measures. Innovative approaches to infrastructure financing and government encouragement of private capital participation were required to boost infrastructure finance and bridge the investment gap.16 Investing in Power Plants

The value-added chain for thermal (fossil fuel) power plants was simple in concept. In operations, fuel was needed. In Africa this was typically coal, natural gas, or diesel. The fuel was either burned in a furnace to generate steam to turn a turbine that rotated an armature that generated electric current, or the fuel was burned in a reciprocating engine similar to a diesel truck motor to turn an armature to generate electric current. The electric current departed the facility through high voltage transmission lines. Operating risks included cost and availability of fuel, operating and capital replacement costs, and price and quantity of electricity sold (“offtake” risk). For many projects the “offtake risk” was the big unknown: for a plant with a life span of decades, would the price and quantity purchased (and paid for) be sufficient to cover costs and investment?

The inception and delivery of power facilities had clear phases. In the inception phase all of the technical designs, land acquisition, operating permits, and financial arrangements had to be made. This could take years and be very expensive and there was substantial “dead deal” cost if a project did not go forward. At the end of the inception phase, a milestone generally called something like “financial close,” project construction and delivery started in earnest. When construction was concluded, and the facility was commissioned to operate, a milestone called something like “in service” or “substantial completion” was reached. (The construction phase also was fraught with unknowns ranging from unforeseen underground conditions to cost overruns to land rights protests). This began the operations phase of the facility. Following several years of operations, financial investors might seek to liquidate their investment and convey their interest to new investors. Following several decades of operation, the plant would eventually be de-commissioned or undergo material refurbishment, and this would be a liquidation phase.

Many local, state, and federal governments around the world financed, owned, and operated their own electric power facilities. This tended to be the case when the offtake risk was contained and the price for power was reflective of the fully loaded cost of power (both operating costs and a return on the original capital). This route also required that the government entity have access to capital to build a plant that could cost more than a billion dollars.

In many other areas of the world the local government did not have access to this kind of capital, or to the design, construction, and operating expertise to finance and build a large capital project. Many configurations to address this issue were in place around the world. Some of the most frequent included:

Independent Power Producer (IPP)IN this model the facility was financed, built and run by a separate entity. Output was then sold to an offtaker, usually a government entity, usually under a Power Purchase Agreement (PPA). The arrangement could have a very long duration. Build Operate Transfer (BOT)IN this model, the plant was built and operated by an IPP company for a fixed amount of time after which the plant was transferred to the government. The IPP had to receive tariff revenue from the PPA sufficient to both cover operating costs and repay the original investment for this to be attractive. If all initial capital was also raised by the IPP company, this was commonly called a finance, build, operate, transfer (FBOT).

In the IPP, BOT and FBOT models, the offtake terms were dictated by the power purchase agreement (PPA) so that the privatizer did not bear revenue risk.

Public Private Partnership (PPP) Another variety of project was the PPP where the privatizer performed some or all of the roles performed in the IPP and BOT models and also participated in revenue upside and downside, usually influenced by a tariff that could be charged and volume of electricity that could be sold at that tariff.

Pension Funds as a Source of Infrastructure Finance

Pension funds acted as an important source of capital infrastructure investment in many parts of the developing world, with varying oversight and mixed results.17 Pension fund reform and regulations in several African countries, including Nigeria, had resulted in the rapid growth of pension fund assets as individuals and families came into the middle class, generated savings to invest, and started to plan ahead for future financial needs. By the end of 2017, the total assets of pension funds in Nigeria stood at 7.4 trillion Naira. A significant amount of this capital could potentially be directed toward local investment in infrastructure.18

Pension funds and life insurance companies had similar long-term obligations to pay out benefits to pensioners and policy holders. Revenue-producing infrastructure elements like power plants and toll roads were long lived assets, so there was a chance to match tenor of liabilities and assets. Operators had an opportunity to raise infrastructure tariffs with inflation, providing added benefits to some fund investors (depending on the form of the security). The incoming pension investment funds were received from individuals in Naira, the payouts would be in Naira, and infrastructure assets collected tariffs, tolls, and fees in Naira. In theory, it would make a lot of sense for long term managers like pension funds to invest some of their portfolios in locally denominated long term safe assets like infrastructure. This could be a transformational new source of capital in Nigeria and in Africa, in contrast to traditional power or toll road investments denominated in US dollars or euros (and with borrowings from large international investors also denominated in US dollars or euros, with all of the cautions, constraints, hedges, and restrictions those arrangements entailed).

READ ALSO: Fashola beating a new path in higher institutions infrastructure

To date, infrastructure securities in Nigeria had not been felt safe enough – or high yielding enough – for retirement or life insurance asset managers. Therefore, in spite of the conceptual appeal, due to a number of barriers pension fund investment in infrastructure was slow in many countries, including Nigeria. See Exhibit 7 for a discussion of some of these barriers.

The Nigerian government had long sought to encourage pension fund investments in infrastructure. In 2016, the country’s Minister of Power, Works and Housing, Babatunde Raji Fashola, called for Nigeria’s sizable pension fund assets to be used in building highways, ports, hospitals and other significant infrastructure.19 However, the lack of available projects that complied with Pencom regulations for pension fund investments in infrastructure had been an impediment to such investment.

Pencom Regulation on Investment of Pension Fund Assets of April 2017 (Pencom Regulations) established requirements to be met for Nigerian pension fund assets to be invested in infrastructure. These included that projects have a minimum value of 5 billion Naira (approximately US$13.85 million), be awarded to concessionaires with good track records through a transparent and open bidding process, and that any bonds issued to fund infrastructure projects have robust credit enhancements. See Exhibit 8 for the relevant sections of the Pencom Regulations. The absence of eligible transactions and credit guarantees for related bonds had historically been a significant obstacle.

The arrival of Infracredit had the potential to completely change this. As noted by Azubike:

We were established as a local currency credit investment facility with the mandate to catalyze long term local currency financing for infrastructure using our guarantees to improve the credit quality of what we considered eligible infrastructure assets meeting our criteria. Lending our guarantees to these transactions improves their creditworthiness and ratings to be able to attract pension funds as investors in this asset class. Nigerian pension funds are authorized to invest up to 35% of their assets in corporate bonds, including 15% in infrastructure bonds and corporate bonds and that translates to about $US 6 billion dollars in Naira equivalent but they have almost no investment in that asset class compared to the industry’s total assets under management. When pension funds were asked why they do not allocate funds to infrastructure, one of the key reasons given was limited asset classes to invest in and a reluctance to take on credit risk for the infrastructure asset class which they don’t understand. So, part of Infracredit’s mandate is to help steer that long-term capital into infrastructure.20

Although pension fund assets were viewed as an important potential source of infrastructure investment, they were susceptible to improper use. Nigeria, as discussed in more detail below, had experienced problems with mis-appropriation and mismanagement of pension funds. Other emerging market countries around the world, including Argentina, Brazil and South Africa have all had to manage challenges in ensuring proper investment of these significant potential sources of infrastructure finance.