Since Nigeria’s return to democracy in 1999, hardly has the job of leading Africa’s most populous nation been as demanding as it is today, with the single most daunting task being to pull the world’s poverty capital from the brink of a socio-economic implosion.

The poor state of Nigeria’s economy is largely playing in the mind of electorates ahead of crucial votes Saturday, February 23.

Nigeria’s next leader may not be able to paper over the cracks of a weak economy. Not when there aren’t sufficient petrodollars to call on.

Many of Nigeria’s leaders of old have managed to keep the economy trudging along with bad policies if oil prices stayed high and production was stable. But not anymore.

The problem is that while oil production has more or less stagnated in the last decade, the population has steadily climbed and by 2040, Nigeria will be the third most populous nation in the world with a population of 400 million.

This means the country’s oil revenue per capita is shrinking along with the country’s oil wealth.

If the last three and a half years are anything to go by, then the days of a leader managing to paper over the cracks of a bleeding economy amid dodgy policies are over.

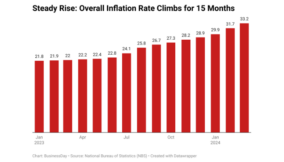

The next president must salvage what’s left of a broken economy that is home to the largest concentration of people globally living below $2/day (87 million or 44 percent, according to a 2018 Brookings Institution report) and tainted with underwhelming growth that is below population growth rate, falling company profits and record unemployment rate of 23 percent.

That figure is closer to 50 percent when underemployment is factored in.

India, which Nigeria overtook on its way to becoming the poverty capital of the world, has 57 million people that are extremely poor, representing just 4.4 percent of its 1.3 billion population.

The next president will need to deliver on economic growth of 10 percent if the country is to create sufficient jobs for its teeming population and lift the majority of its people out of poverty. Growth in the 10 percent region is largely uncharted territory for Nigeria since 1999.

Surely, the world would be watching to see what the next president does to achieve double-digit economic growth and shared prosperity.

“Our current economic growth can’t solve our challenges as unemployment and inflation are still at double digits while poverty is increasing,” says Gbolahan Ologunro, an equity research analyst at Lagos-based CSL stockbrokers.

“The critical sectors in the economy are still struggling and much work needs to be done in terms of lifting the real sectors and putting them on the path of sustainable growth path,” he adds.

Insecurity, high interest rates and unstable power are some of the major constraints to the real sector, whether its manufacturing or construction, and they have grown worse over time.

Only 23 percent of businesses in Nigeria can get needed financing, according to the Manufacturers Association of Nigeria (MAN).

For those businesses that manage to get bank credit, it is often expensive, with the benchmark monetary policy rate sitting at 14 percent for almost two years.

The central bank’s lending rate to commercial banks in South Africa is 6.5 percent, while the prime lending rate (lending rate to customers) is 10 percent. Kenya’s determining and lending rates are 9.5 percent and 13.5 percent, respectively, while Ethiopia’s is 5 percent.

How Nigeria’s next leader addresses this will be telling on households and businesses.

The next president would also assume power when public revenues are low and the budget deficit is widening. A dark time when the government commits over 60 percent of each naira in revenue to debt servicing and the bulk of the remaining cash on payment of workers’ salaries and other overhead costs that come with an over-bloated civil service.

At the end, it means there is little or nothing left for capital spending in a country where a yawning infrastructure deficit has undermined economic growth and tormented businesses.

The Africa Development Bank estimates that Nigeria needs to spend $100 billion annually over the next 30 years to get its infrastructure at par with what is needed. In the last three years combined, the government has spent only $10 billion on capital projects, which works out to $3.3 billion annually, 3 percent of the required investment.

That’s despite Nigeria spending more in that three-year period in naira terms as the government boosted capital spending on projects from roads to rail. What this implies is that the government’s record spending is not enough to make a dent on the nation’s infrastructure needs. And it’s no hidden secret.

“The reality on ground is that the government alone cannot finance the infrastructure gap in the country which has made it difficult to achieve sustainable development,” Ebrima Faal, senior director of AfDB, told BusinessDay.

Surely, the next president has his work cut out in changing the current funding mix and attracting sufficient private capital to fix the infrastructure challenges.

He must also improve on puny government revenue which at 6 percent of GDP is one of the lowest globally. He must at least put up a good fight to achieve the emerging market average of 15 percent of GDP.

Charles Robertson, chief economist at Moscow-based investment bank, Renaissance Capital, says the next president must also tackle rising adult illiteracy, fast-track industrialisation and diversification, double investment to GDP and deliver a more competitive currency.

Robertson thinks the current market rate of the naira is overvalued by 20 percent.

There’s no denying the fact that Nigeria needs a leader with a bold plan to open up the economy to an infusion of cash, which it has severely lacked in the past four years.

The next president will also have his hands full with an underperforming agriculture sector that contributes the single most of any sector to Nigeria’s GDP.

Agriculture GDP grew 2.12 percent in 2018, the slowest pace in 26 years, despite the blend of agriculture programmes such as Anchor Borrowers’ Programme, Agricultural Credit Guarantee Scheme Fund, Commercial Agriculture Credit Scheme, and Bank of Agriculture Loans implemented by the authorities over the years.

While the initiatives are positive, there were production drawbacks caused by herdsmen/farmer crisis and consequent trade route disruptions. In addition to insecurity, there were reported cases of late disbursements and inadequacy of funds. These setbacks largely limited the agriculture GDP growth in 2018.

There are more hurdles ahead for Nigeria’s next leader from the herder-farmer clashes north of the country and militants constantly threatening to blow up oil pipelines south of Africa’s largest oil producer.

He may take comfort in relatively high oil prices, but if the militants make good their threats to resume damaging oil pipelines, lower production volumes threaten to scupper any gains.

Whoever emerges the next president in Saturday’s polls, which pits incumbent President Muhammadu Buhari of the APC against Atiku Abubakar of the PDP, it only gets tougher from there on.

So delicate is the next president’s job that he risks drawing the ire of a largely socialist and illiterate population if he is to execute the tough reforms required to set Africa’s biggest economy on the path of robust growth.

LOLADE AKINMURELE